![[Editorial] 30 years later, is apartheid really over?](https://lejournaldelafrique.com/wp-content/uploads/2021/06/caricature-jda-apartheid-360x180.jpg)

![[Edito] Gabon and Commonwealth: the whims of Prince Ali](https://lejournaldelafrique.com/wp-content/uploads/2021/06/caricature-JDA-Bongo-360x180.jpg)

![[Editorial] Facebook and Twitter, more dictators than dictators?](https://lejournaldelafrique.com/wp-content/uploads/2021/06/Caricature-JDA-FB-TW-360x180.jpg)

![[Edito] Rwanda: for the French apologies, we will have to go back](https://lejournaldelafrique.com/wp-content/uploads/2021/05/Caricature-rwanda-JDA-360x180.jpg)

![[Edito] Guinea: Alpha Condé, the oppressed turned oppressor](https://lejournaldelafrique.com/wp-content/uploads/2021/05/Caricature-Alpha-Conde-360x180.jpg)

![[Edito] CFA Franc: a facelift cut to measure for France](https://lejournaldelafrique.com/wp-content/uploads/2021/05/Caricature-JDA-CFA-360x180.jpg)

![[Edito] Riyad Mahrez: One, two, three, viva l'Algérie!](https://lejournaldelafrique.com/wp-content/uploads/2021/05/caricature-Mahrez-360x180.jpg)

![[Edito] Niger: Mohamed Bazoum begins a delicate balancing act](https://lejournaldelafrique.com/wp-content/uploads/2021/04/image_6483441-1-360x180.jpg)

If the conflict gets bogged down, the situation could become untenable for countries in North Africa and the Middle East that depend on Russian and Ukrainian grain exports.

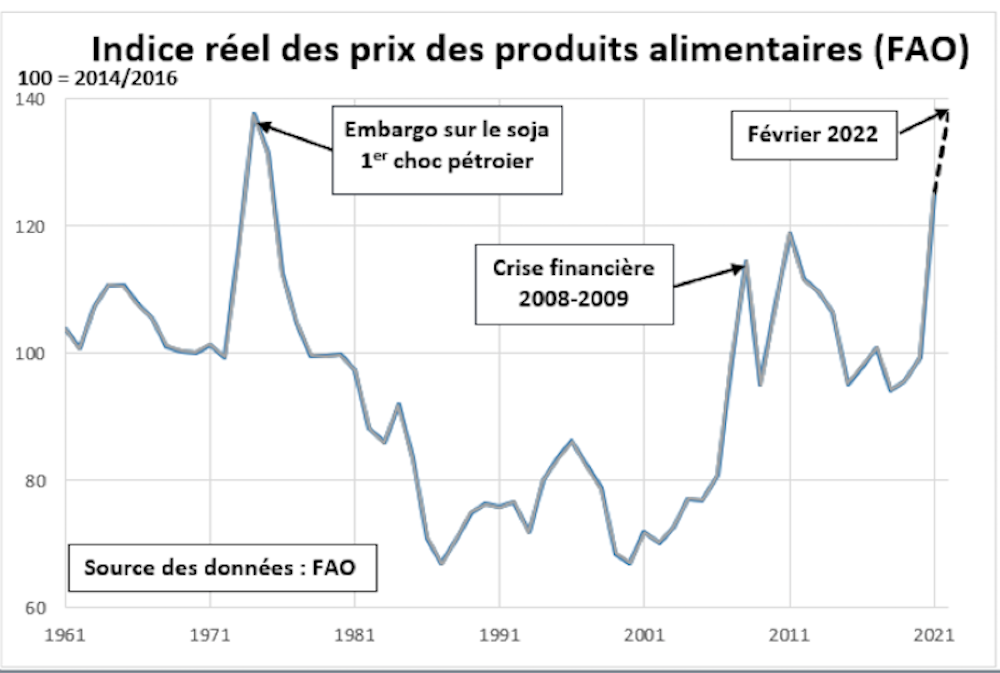

The outbreak of war in Ukraine abruptly halted all grain and oilseed exports from Ukraine and a large proportion of those from Russia transiting through the Black Sea. The interruption caused a surge in the prices of wheat, corn and oilseeds, three major components of commodity price index calculated by the FAO since 1961.

For 60 years, access to basic foodstuffs has never been so costly in real terms. This agricultural inflation will deal a very severe blow to food security in the world.

The cost of basic foodstuffs at an all-time high

Expressed in purchasing power relative to industrial goods, the price of these agricultural materials exceeded in March its historic high reached during the 1973 crisis, when the United States imposed its embargo on soybeans and OPEC on oil. This surge in prices is likely to continue.

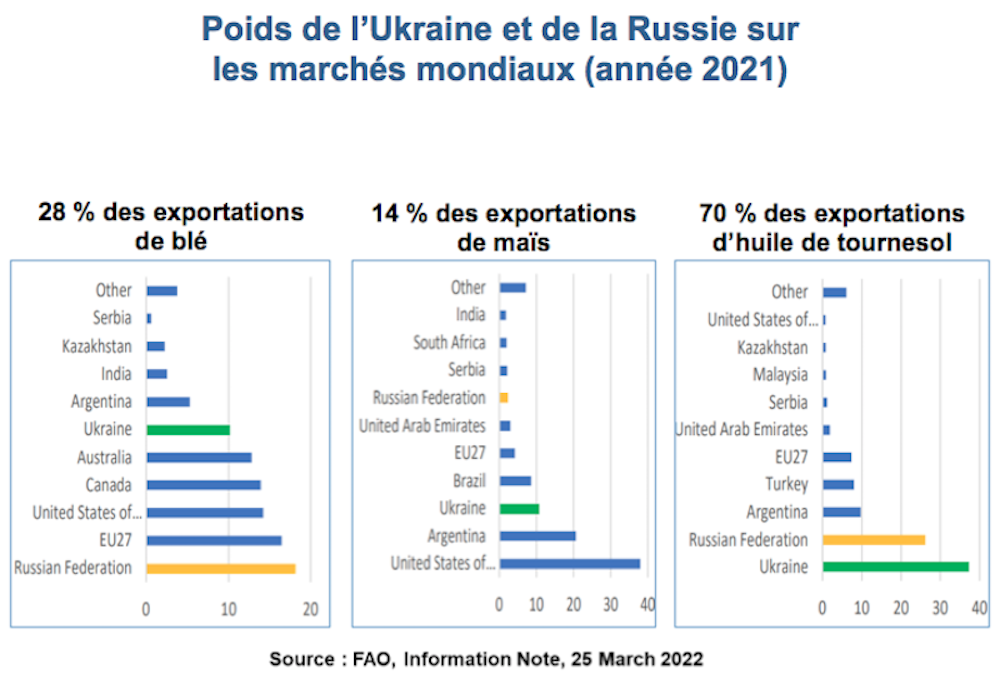

With a quarter of the harvest passing through international trade each year, wheat is by far the most traded cereal in the world. Russia and Ukraine provide just under 15% of world production and nearly 30% of exports.

Before the start of the war, Ukraine – which reaped a record harvest in 2021 – had in its silos the order of 6Mt of wheat for export and Russia about 8Mt. These flows are mainly intended for North Africa and the Middle East, which are among the world's major buyers. Substitutes must be found for them, which does not pose a problem of short-term availability, given world stocks, but exerts pressure on prices unknown in times of peace.

The great uncertainty concerns the next campaign which starts in July 2022. If shipments do not restart quickly, the silos will not be available to harvest the summer harvest. The most dramatic situation would be when the next Ukrainian harvest would be hampered by the continuation of the conflict. Global stocks will not fill such supply disruptions for long and, in the short term, there is little untapped production potential in the world.

Spring 2022 sowing uncertainties

The impacts on the maize market depend mainly on Ukraine, which supplies each year around 15% of the world market, while Russia is a secondary exporter. The situation on this market is tighter than that of wheat, following the droughts that affected production in Brazil and Argentina.

For maize, the first question relates to the sowing which is carried out in the spring of 2022 (April-May) for a harvest in the fall. If the war prevents sowing, the world corn market, already very tight, will not be able to compensate for the lack of deliveries from Ukraine with, in prospect, an additional increase in the cost of animal feed and difficulties for the food supply. in Latin America.

Ukraine is finally the world's largest exporter of sunflower oil. With Russia, it controls the half of world seed production and around 70% of exports (seed + oil). Sunflower ranks far behind soya and oil palm on the world oilseed market, but plays a significant role in Europe for edible oils and cakes intended for livestock feed.

As with all oilseeds, the market is already very tight and the uncertainties about spring sowing in Ukraine are the same as for corn.

A dangerous spiral of rising agricultural prices and costs

Beyond its direct effects on the global grain supply-demand balance, the Ukrainian conflict has triggered a spiral of rising agricultural production costs.

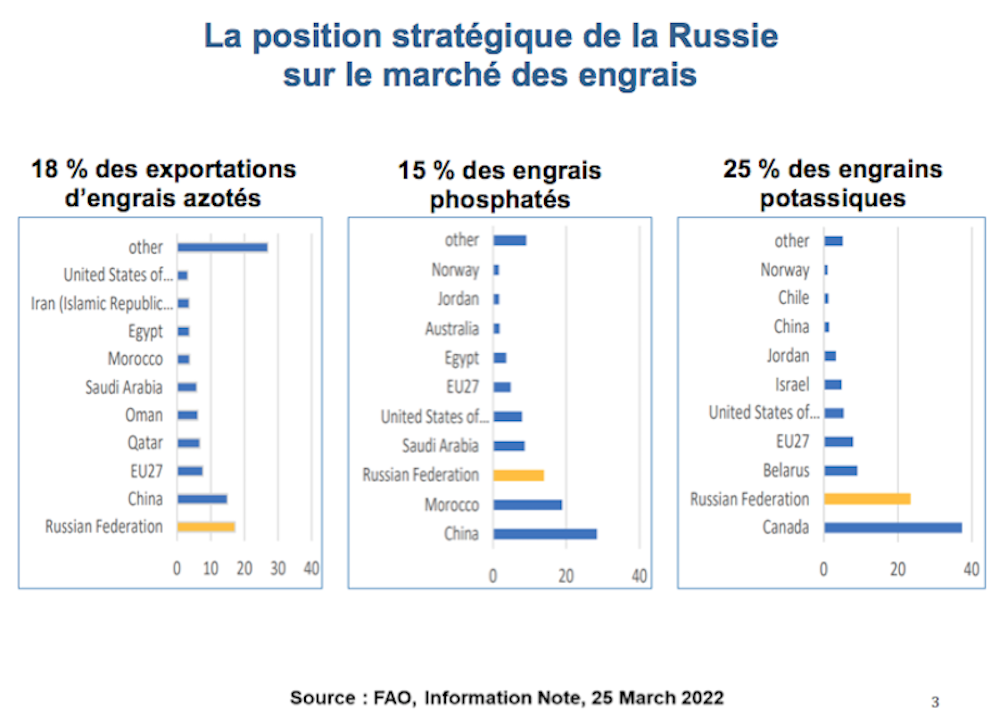

Russia is the world's largest fertilizer exporter, with a strong position on nitrogen fertilizers or on the components used to manufacture them (ammonia and ammonium nitrate). Together with its Belarusian ally, it also dominates the market for potash-based fertilizers.

If deliveries of these products are slowed down or suspended within the framework of Western sanctions, the already observed increase in the price of these products will increase. It will be difficult for the big importers of nitrogenous fertilizers (Brazil and Argentina) to find alternatives to flows coming from Russia.

Finally, the price of fertilizers is directly correlated to that of gas and to a lesser extent to that of oil. As shown by a recent analysis of the FAO, this correlation is practically instantaneous between nitrogenous fertilizers and natural gas which can represent up to 80% of their manufacturing cost. A rise in the price of natural gas affects nitrogen fertilizers used all over the world, the market being global.

The war in Ukraine is fueling a dangerous spiral of rising agricultural prices and costs. This upward spiral is a powerful propagator of inflation around the world.

The inevitable rise in food prices

The conflict will contribute to the acceleration of inflation, via its double impact on energy and food prices.

Soaring grain prices take longer to trickle down to retail than soaring energy prices, as food products are heavily processed. In a 250 gram baguette displaying a little less than €1 at the bakery, the wheat used weighs no more than 10 cents. Once “in the pipes”, the spiral of rising food prices, on the other hand, affects the household budget more heavily than that of energy.

In France, food (excluding alcoholic beverages and catering outside the home) accounts for some 11% of household spending, twice as much as energy purchases. The acceleration in food prices was observed there in March 2022 with a increase of 2,8% over one year and 7,2% if we remove processed products. This acceleration will continue.

In developing countries, food is by far the largest item of family expenditure. In sub-Saharan Africa, it weighs on average for 40% of family budget and much more in those with low incomes. This is why the increase in the price of basic agricultural products threatens food security.

Food security threats

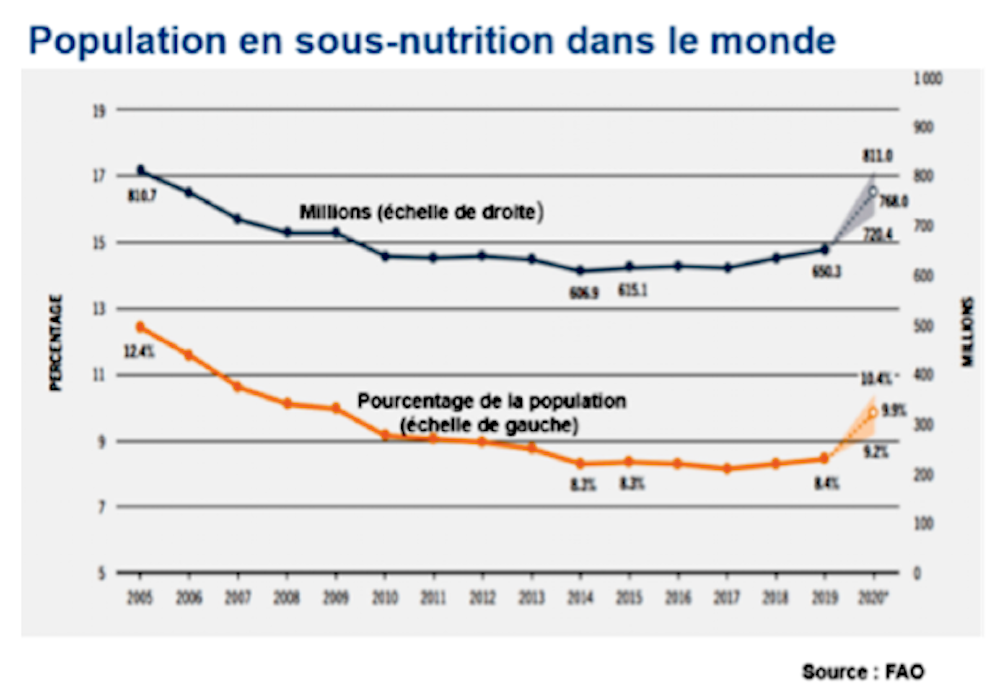

At the start of the war, the FAO estimated about 810 million the number of hungry people in the world. After three decades of decline, this number stabilized during the 2010 decade, to rise in 2020 and 2021 under the impact of Covid.

In his first analyzes, the FAO estimates that the Ukrainian conflict could lead to an additional increase of around 7 to 13 million people in a situation of undernutrition this year, mainly in Asia-Pacific and in Africa south of the Sahara.

The risk is particularly high in countries that are both grain and energy importers. The double shock is in fact likely to destabilize their balances of payment by limiting their ability to purchase food on the international market. Moreover, rising international prices are dangerously increasing the fiscal costs of retail price subsidies in countries like Egypt and Iran.

Medium-term prospects

A first uncertainty relates to the functioning of international markets, where strategic behavior risks aggravating the inflationary spiral. This is why both the FAO and the European initiative " Food and agriculture resilience mission (FARM), announced by Emmanuel Macron at the recent G7 summit, call for increased surveillance of these markets.

But behind the declarations of intent, it is difficult to discern the means of action. The European Union has dismantled its means of intervention and has no strategic food stocks. At the global level, there is no concerted inventory management system to regulate the markets.

In such a context, major exporters are tempted, like Argentina or Russia, to slow down or block part of their exports by favoring their domestic market. The multiplication of this type of action can only accentuate the international tension of the courses.

In the absence of preventive regulation, the only curative action will be to increase emergency food aid, which will have to be financed at a high price, with the risk of destabilizing local agricultural markets.

However, the surest way to curb the food crisis is through a revival of food production in the countries of the South, which cannot take place without strong protection for agricultural holdings in the face of international markets.

Christian from Perthuis, Professor of Economics, founder of the “Climate Economics” chair, Paris Dauphine University - PSL

This article is republished from The Conversation under Creative Commons license. Read theoriginal article.